Financial Planning

A baby boomers’ 66th birthday means more than blowing out a lot of candles.

As far as Social Security is concerned the date is a landmark, and many of the program’s critical features and benefits are linked to this age. Accordingly, advisers and their clients need to understand the options and choices available in order to maximize Social Security benefits and retirement income plans.

There are three milestone ages in the Social Security retirement program: 62, 66 and 70. The earliest age at which one is eligible to file for benefits is 62. Workers can’t delay filing for benefits past age 70.

Between these two dates is the all-important Full Retirement Age (FRA), which for the vast majority of baby boomers is 66. For those born before 1955 FRA will be exactly on their 66th birthday. For those born between 1955 and 1959 it will be later in their 66th year.

Here are four important program features that hinge on age 66:

Basic Benefit Regardless of the age at which a person files for benefits, their actual benefit amount is calculated based on the age 66 FRA value.

File for early benefits (between 62 and 66) and clients will see their benefit amount calculated as a reduction from the age 66 value. File later (delay filing) and their age 66 benefit is increased by 2/3 of 1% for each month beyond their 66th birthday that they wait before filing.

Earnings’ Test The earnings’ test both confuses and irritates beneficiaries of Social Security. This feature may cause a portion (or even all) of retirement benefits to be withheld if the Social Security beneficiary is younger than FRA and is still working.

Here’s how it works. $1 of Social Security benefits are withheld for every $2 of earned income over $16,920 for clients between ages 62 and 65. $1 of benefits is withheld for every $3 of earned income over $44,880 in the year that a client turns 66. When a recipient reaches full retirement age (66) the earnings’ test goes away and no benefits are withheld regardless of income earned.

One important caveat is that any withheld income is actually paid back in the future. An actuarial adjustment will be made at age 66 increasing a client’s benefit in order to distribute the withheld income.

Beware that some beneficiaries still will not be satisfied since they don’t perceive the value of the adjusted benefit paid out over the remaining lifetime as equivalent to the recently withheld benefits.

Do Over At 66 beneficiaries have a new option to second-guess their filing choices.

Some clients regret their decision to file for early benefits. They may have gained a new source income or assets, perhaps through an inheritance. They may have learned more about the mechanics of the Social Security system and realized the potential benefits of delaying filing and collecting a higher lifetime benefit. In either event, they may wish to change their decision to file. There are two mechanisms by which they can suspend benefits which have already started.

The first choice is available only during the initial 12 months after benefits begin. During that time beneficiaries may withdraw their application for benefits but must repay all benefits collected. At that point their future potential benefits will continue to grow as if they had never filed before.

The second choice is only available once a person reaches age 66. At age 66 or later one can suspend benefits. In this case no repayments are required. Future benefits will then grow at 8% per year, based on the benefit value when it was suspended, until age 70 years.

Restricted filing Perhaps the most widely discussed feature unique to age 66 is the ability to use the Restricted Filing option. This special option is being phased out for younger applicants but is still available to anyone born before Jan 1, 1954.

Once a client is at least 66 they can file for Social Security benefits restricted to spousal benefits only. This is a benefit based solely on the work history of their spouse. Simultaneously the Social Security benefit based on their own work history continues to accrue valuable delayed retirement credits of 8% for each year until as late as age 70.

This powerful strategy can provide both higher family lifetime benefits for a couple and, very importantly, maximizes the benefit that the survivor will receive when the first spouse passes away.

Many consequential Social Security choices hinge on the pivotal age of 66. Keep these in mind and help your clients take full advantage of these important options.

– Article from Financial-Planning.com

The brokerage industry is largely shifting towards zero-commission trades. On the surface, this would appear to be for the benefit of investors, but there are hidden costs to zero-commission trades.

This shift creates several questions investors should contemplate.

How are brokerages replacing their primary source of revenue?

Are brokerages switching to zero-commission trades to benefit investors?

There are two primary ways brokerages profit from zero-commission trades.

1. Rounding Up the Cost Per Share

When an investor places a trade, the cost per share is rounded up adn teh increase in cost is incurred by the unaware investor.

2. Selling Order Flows

When an investor places a trade, their order information is sold to a third-party (typically high-frequency trading firms). This deteriorates the order execution, resulting in higher purchase prices adn lower sell prices. The firms purchasing order flows can manipulate teh market and improve their own order execution.

“Payments for order flow may result in lower quality order execution, leading to slightly higher buy prices and marginally lower sell prices (for investors).” Investopedia

Notable brokerages that sell order flows:

- Robinhood

- E-trade

- Vanguard

- Charles Schwab

- TD Ameritrade

“Data from Alphacution shows taht revenues from payments for for order flow almost trpled at the four major brokerages – TD Ameritrade, Robinhood, E-trade (MS), Charles Schwab (SCHW) – to $2.5 billion in 2020 from $892M million in 2019.” Yahoo

After months of negotiations, a new tax and spending bill was approved by Congress and signed into law by President Trump on July 4. This new budget is far-reaching, it makes many parts of the Tax Cuts and Jobs Act permanent, it raises state and local tax exemptions, extends the estate tax limits, and much more. It attempts to offset some of these provisions with spending cuts in areas such as Medicaid.

While trade policy has been at the forefront over the past several months, tax and spending policy in Washington has been a growing source of uncertainty for many years. While there is political disagreement regarding this new budget, most importantly, it does take the possibility of a “tax cliff” off the table. Without this bill, tax policy could have changed dramatically at the end of this year when provisions were set to expire.

The new bill, dubbed the “One Big Beautiful Bill” by the administration, extends and expands several aspects of the 2017 Tax Cuts and Jobs Act (TCJA) that were set to expire. It also introduces new measures that provide other benefits to taxpayers. These measures are partially offset by spending cuts in other areas. Here are just some of the major provisions that may affect households:

- Current TCJA tax rates and brackets are now permanent. They were originally set to expire at the end of 2025.

- The standard deduction increases to $15,750 for single filers and $31,500 for joint filers in 2025.

- There is an additional $6,000 deduction for qualifying seniors (sometimes referred to as a “senior bonus”) that phases out for gross incomes exceeding $75,000. The provision expires in 2028.

- The alternative minimum tax exemption is now permanent. It also increases phaseout thresholds to $500,000 for single filers, which will be indexed for inflation in the future.

- The child tax credit rises from $2,000 to $2,200 per child, with future adjustments indexed to inflation to maintain purchasing power over time.

- The state and local tax (SALT) deduction cap increases to $40,000 from a $10,000 limit with annual increases of 1% through 2029. It is then scheduled to revert back to $10,000 in 2030.

- A deduction for tip income capped at $25,000 annually for workers earning less than $150,000, effective through 2028.

- Some green energy tax credits are repealed, including for electric vehicles and residential energy efficiency credits.

- The federal debt limit increases by $5 trillion. This will prevent Congress from having to debate and approve debt limit increases for some time, reducing political uncertainty.

- For businesses, the bill expands tax breaks designed to encourage domestic investment and job creation.

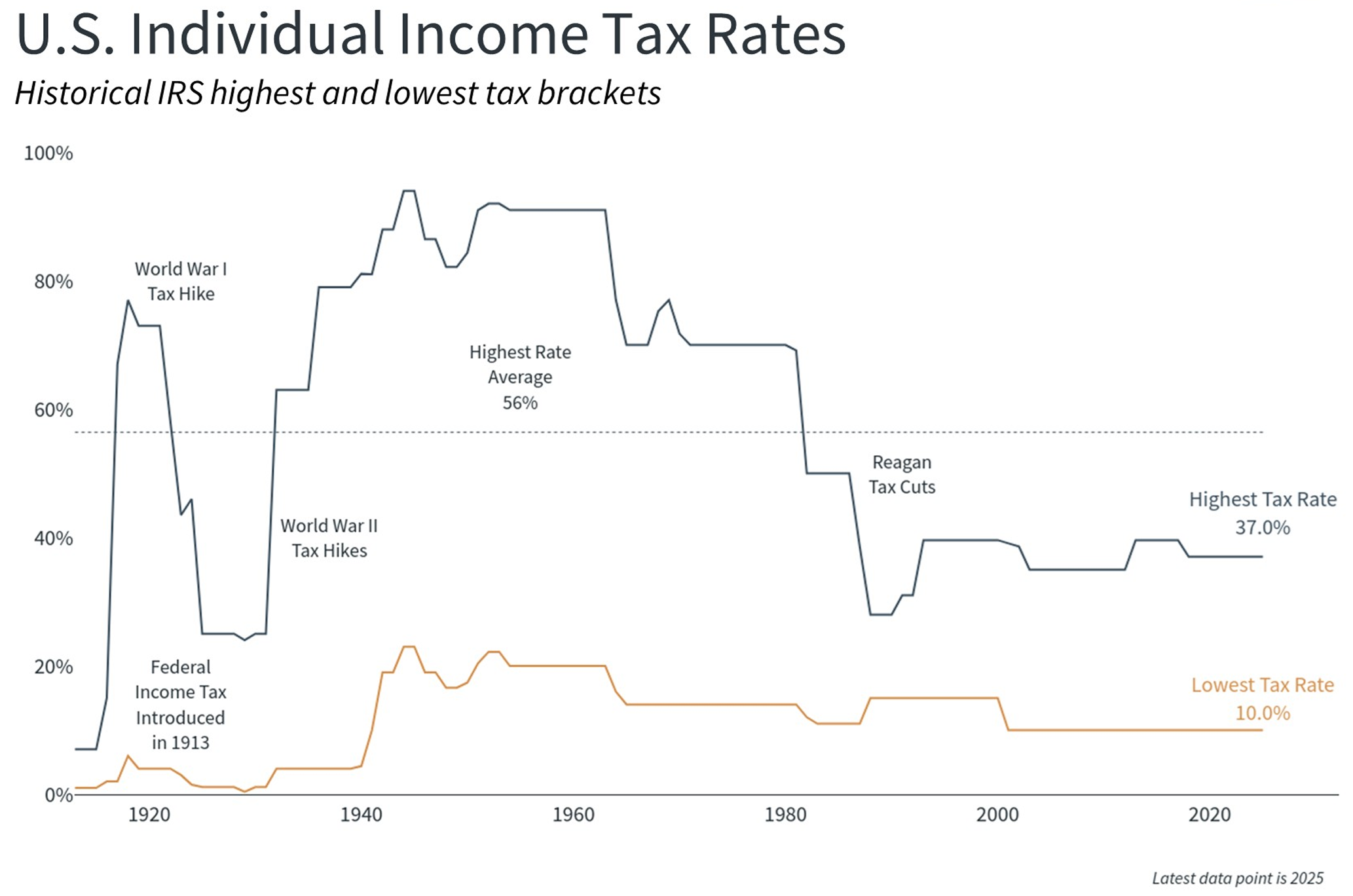

The bill maintains the relatively low tax environment that has characterized the past several decades. As the chart above shows, current tax rates remain below the levels seen prior to the 1980s when top marginal rates exceeded 70%.

Tax cuts decrease government revenues, unless they are accompanied by economic growth that supersedes the cuts. This decrease in revenue needs to be offset by either lower spending or increased borrowing. However, most government spending is for entitlement and defense programs which are politically difficult to change. According to the Department of the Treasury, in 2025 21% of government spending is for Social Security, 14% for Medicare, 13% is for National Defense, and 14% is to pay interest costs on the existing national debt.

Government borrowing has increased persistently over the past century and will likely continue to do so. The Congressional Budget Office estimates that this new tax and spending bill will add $3.4 trillion to the national debt over the next decade. This is against the backdrop of a federal debt that already exceeds 120% of GDP, or $36.2 trillion, which amounts to about $106,000 per American.

Unfortunately, there are no easy political solutions to this challenge. On the one hand, tax cuts improve economic growth, which can help to offset revenue losses through increased economic activity. On the other hand, Washington has a poor track record of balancing budgets even when the economy is strong. The last balanced budgets occurred 25 years ago during the Clinton years, and 56 years before that during the Johnson administration.

There has not always been an income tax in the United States. The modern income tax system began with the 16th Amendment in 1913 which applied modest rates to relatively few Americans. The system expanded dramatically during the Great Depression and World War II, with top rates reaching 94% by 1944. The post-war period brought various reforms, including President Reagan’s Tax Reform Act of 1986 that simplified the tax code and lowered rates.

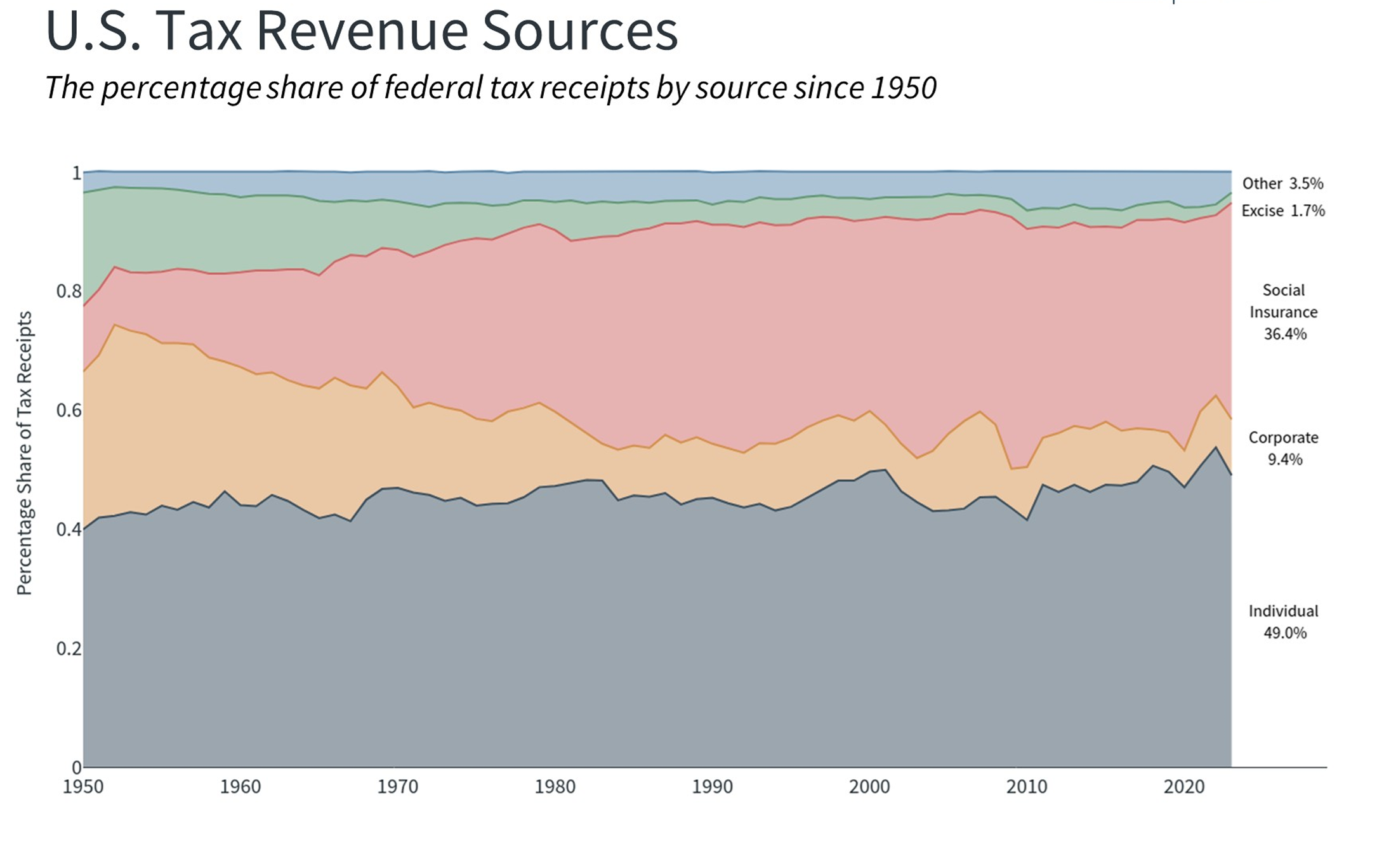

The situation has changed significantly since 1913. The chart above shows, individual income taxes now represent the primary source of federal revenue. Social insurance taxes, also known as payroll taxes, are withheld from wages and help to pay for Social Security, Medicare, unemployment insurance, and other programs. Other sources of revenue are much smaller in proportion and include corporate taxes, which were reduced by the TCJA, and excise taxes, such as tariffs.

For investors, tax policies can have direct implications on financial plans and portfolios. Over longer periods, higher debt levels can influence interest rates and inflation expectations. While these factors have been relatively high in recent years, the worst-case scenarios have not yet occurred. The key for long-term investors is to maintain portfolios that can perform across different fiscal and economic environments.

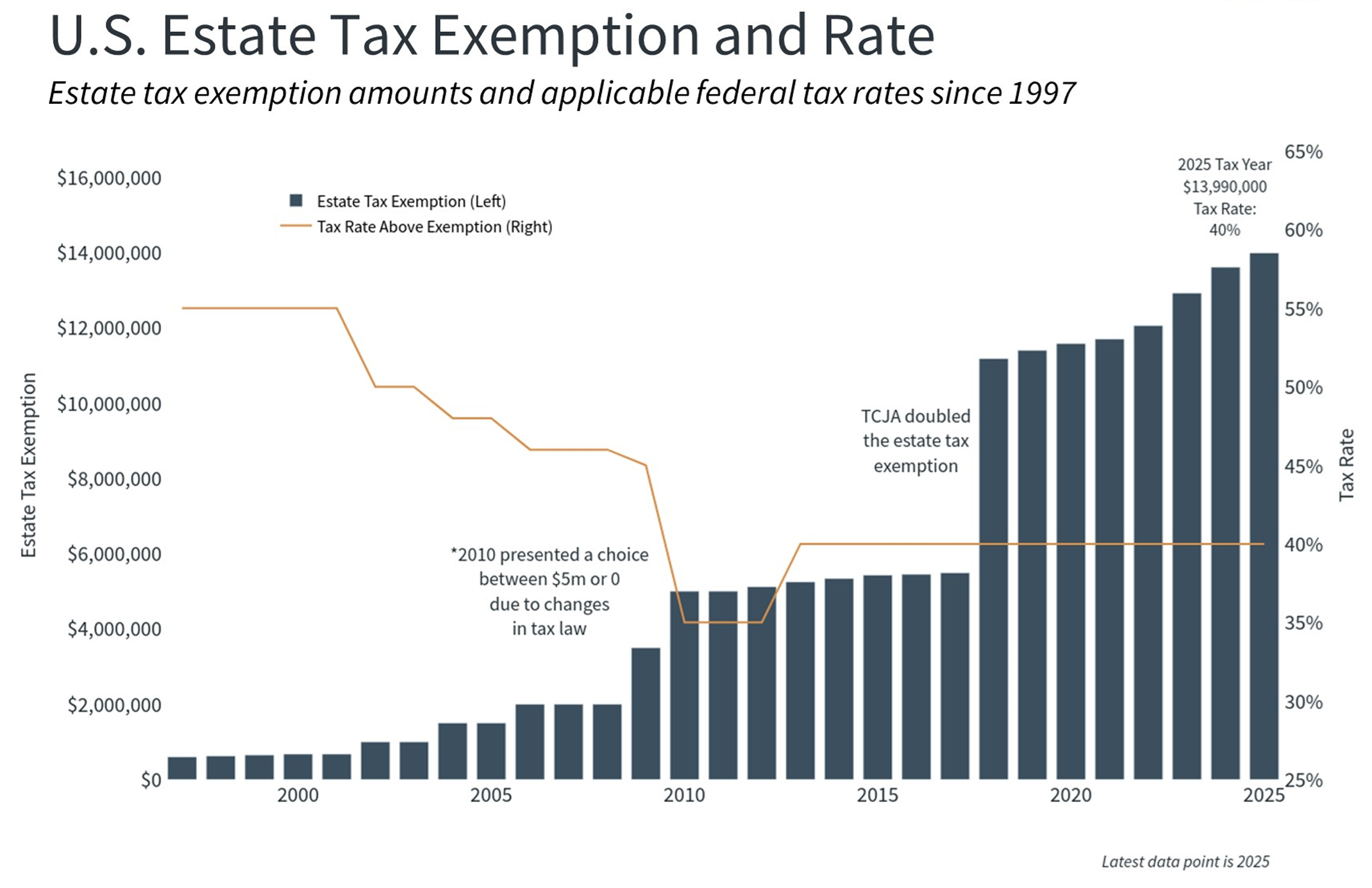

One set of provisions that would have been at the center of a tax cliff is the estate tax exemption. The TCJA doubled these limits which were scheduled to revert to previous levels this year. However, the passage of the new tax bill makes these higher exemptions permanent, further increasing the threshold to $15 million for individuals and $30 million for couples in 2026.

While it may seem like estate taxes only apply to higher net worth households, the reality is that all families must consider how assets can be passed to future generations.

The bottom line? The new spending and tax bill extends and expands the current low-tax environment. When it comes to growing deficits and the national debt, there continues to be no end in sight. The long-term investment implications for these policies are continued inflation, a weakening dollar, and a tailwind for international stocks.

Wyatt Swartz

Written 7/11/2025