The brokerage industry is largely shifting towards zero-commission trades. On the surface, this would appear to be for the benefit of investors, but there are hidden costs to zero-commission trades.

This shift creates several questions investors should contemplate.

How are brokerages replacing their primary source of revenue?

Are brokerages switching to zero-commission trades to benefit investors?

There are two primary ways brokerages profit from zero-commission trades.

1. Rounding Up the Cost Per Share

When an investor places a trade, the cost per share is rounded up adn teh increase in cost is incurred by the unaware investor.

2. Selling Order Flows

When an investor places a trade, their order information is sold to a third-party (typically high-frequency trading firms). This deteriorates the order execution, resulting in higher purchase prices adn lower sell prices. The firms purchasing order flows can manipulate teh market and improve their own order execution.

“Payments for order flow may result in lower quality order execution, leading to slightly higher buy prices and marginally lower sell prices (for investors).” Investopedia

Notable brokerages that sell order flows:

- Robinhood

- E-trade

- Vanguard

- Charles Schwab

- TD Ameritrade

“Data from Alphacution shows taht revenues from payments for for order flow almost trpled at the four major brokerages – TD Ameritrade, Robinhood, E-trade (MS), Charles Schwab (SCHW) – to $2.5 billion in 2020 from $892M million in 2019.” Yahoo

After months of negotiations, a new tax and spending bill was approved by Congress and signed into law by President Trump on July 4. This new budget is far-reaching, it makes many parts of the Tax Cuts and Jobs Act permanent, it raises state and local tax exemptions, extends the estate tax limits, and much more. It attempts to offset some of these provisions with spending cuts in areas such as Medicaid.

While trade policy has been at the forefront over the past several months, tax and spending policy in Washington has been a growing source of uncertainty for many years. While there is political disagreement regarding this new budget, most importantly, it does take the possibility of a “tax cliff” off the table. Without this bill, tax policy could have changed dramatically at the end of this year when provisions were set to expire.

The new bill, dubbed the “One Big Beautiful Bill” by the administration, extends and expands several aspects of the 2017 Tax Cuts and Jobs Act (TCJA) that were set to expire. It also introduces new measures that provide other benefits to taxpayers. These measures are partially offset by spending cuts in other areas. Here are just some of the major provisions that may affect households:

- Current TCJA tax rates and brackets are now permanent. They were originally set to expire at the end of 2025.

- The standard deduction increases to $15,750 for single filers and $31,500 for joint filers in 2025.

- There is an additional $6,000 deduction for qualifying seniors (sometimes referred to as a “senior bonus”) that phases out for gross incomes exceeding $75,000. The provision expires in 2028.

- The alternative minimum tax exemption is now permanent. It also increases phaseout thresholds to $500,000 for single filers, which will be indexed for inflation in the future.

- The child tax credit rises from $2,000 to $2,200 per child, with future adjustments indexed to inflation to maintain purchasing power over time.

- The state and local tax (SALT) deduction cap increases to $40,000 from a $10,000 limit with annual increases of 1% through 2029. It is then scheduled to revert back to $10,000 in 2030.

- A deduction for tip income capped at $25,000 annually for workers earning less than $150,000, effective through 2028.

- Some green energy tax credits are repealed, including for electric vehicles and residential energy efficiency credits.

- The federal debt limit increases by $5 trillion. This will prevent Congress from having to debate and approve debt limit increases for some time, reducing political uncertainty.

- For businesses, the bill expands tax breaks designed to encourage domestic investment and job creation.

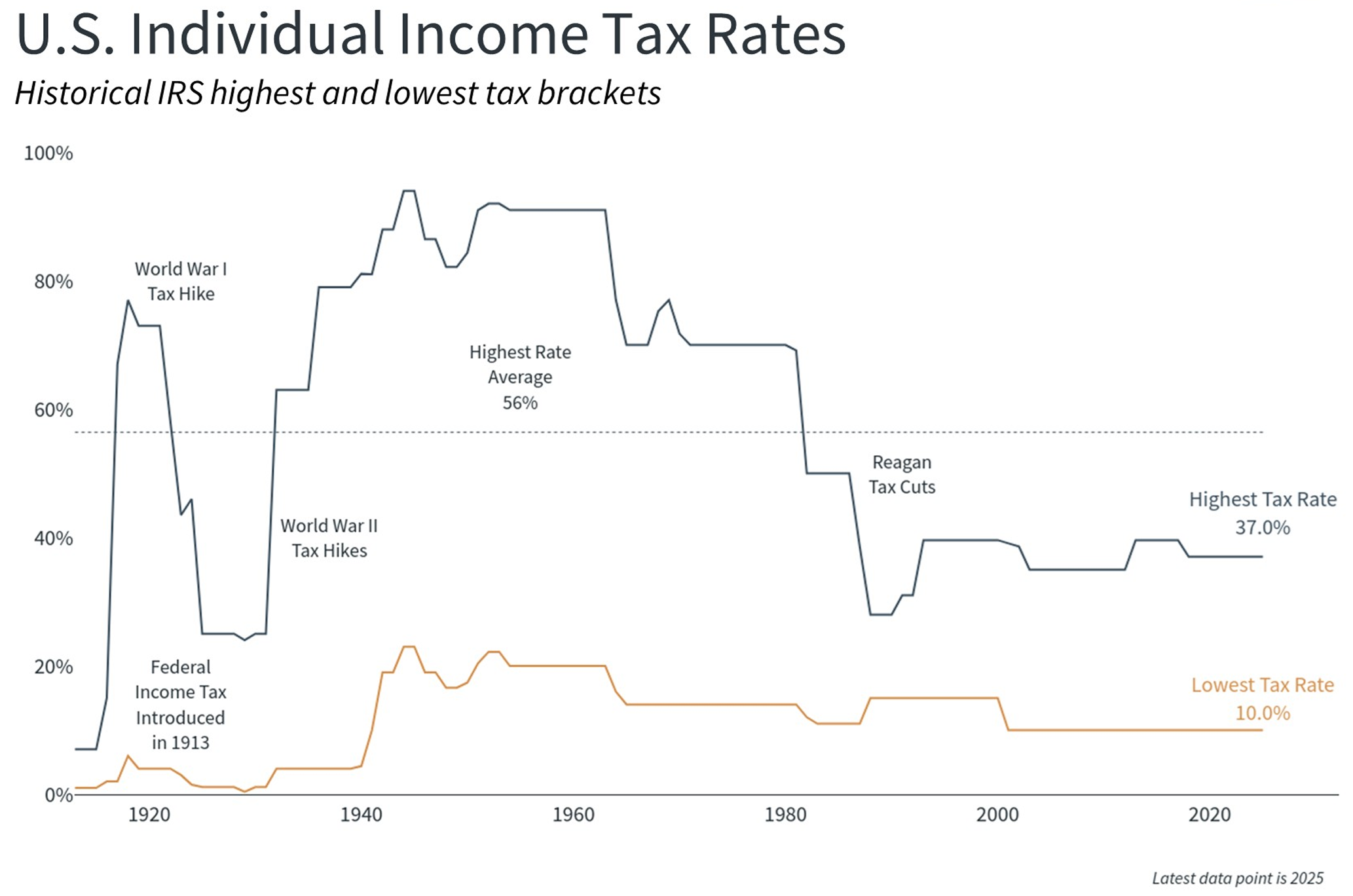

The bill maintains the relatively low tax environment that has characterized the past several decades. As the chart above shows, current tax rates remain below the levels seen prior to the 1980s when top marginal rates exceeded 70%.

Tax cuts decrease government revenues, unless they are accompanied by economic growth that supersedes the cuts. This decrease in revenue needs to be offset by either lower spending or increased borrowing. However, most government spending is for entitlement and defense programs which are politically difficult to change. According to the Department of the Treasury, in 2025 21% of government spending is for Social Security, 14% for Medicare, 13% is for National Defense, and 14% is to pay interest costs on the existing national debt.

Government borrowing has increased persistently over the past century and will likely continue to do so. The Congressional Budget Office estimates that this new tax and spending bill will add $3.4 trillion to the national debt over the next decade. This is against the backdrop of a federal debt that already exceeds 120% of GDP, or $36.2 trillion, which amounts to about $106,000 per American.

Unfortunately, there are no easy political solutions to this challenge. On the one hand, tax cuts improve economic growth, which can help to offset revenue losses through increased economic activity. On the other hand, Washington has a poor track record of balancing budgets even when the economy is strong. The last balanced budgets occurred 25 years ago during the Clinton years, and 56 years before that during the Johnson administration.

There has not always been an income tax in the United States. The modern income tax system began with the 16th Amendment in 1913 which applied modest rates to relatively few Americans. The system expanded dramatically during the Great Depression and World War II, with top rates reaching 94% by 1944. The post-war period brought various reforms, including President Reagan’s Tax Reform Act of 1986 that simplified the tax code and lowered rates.

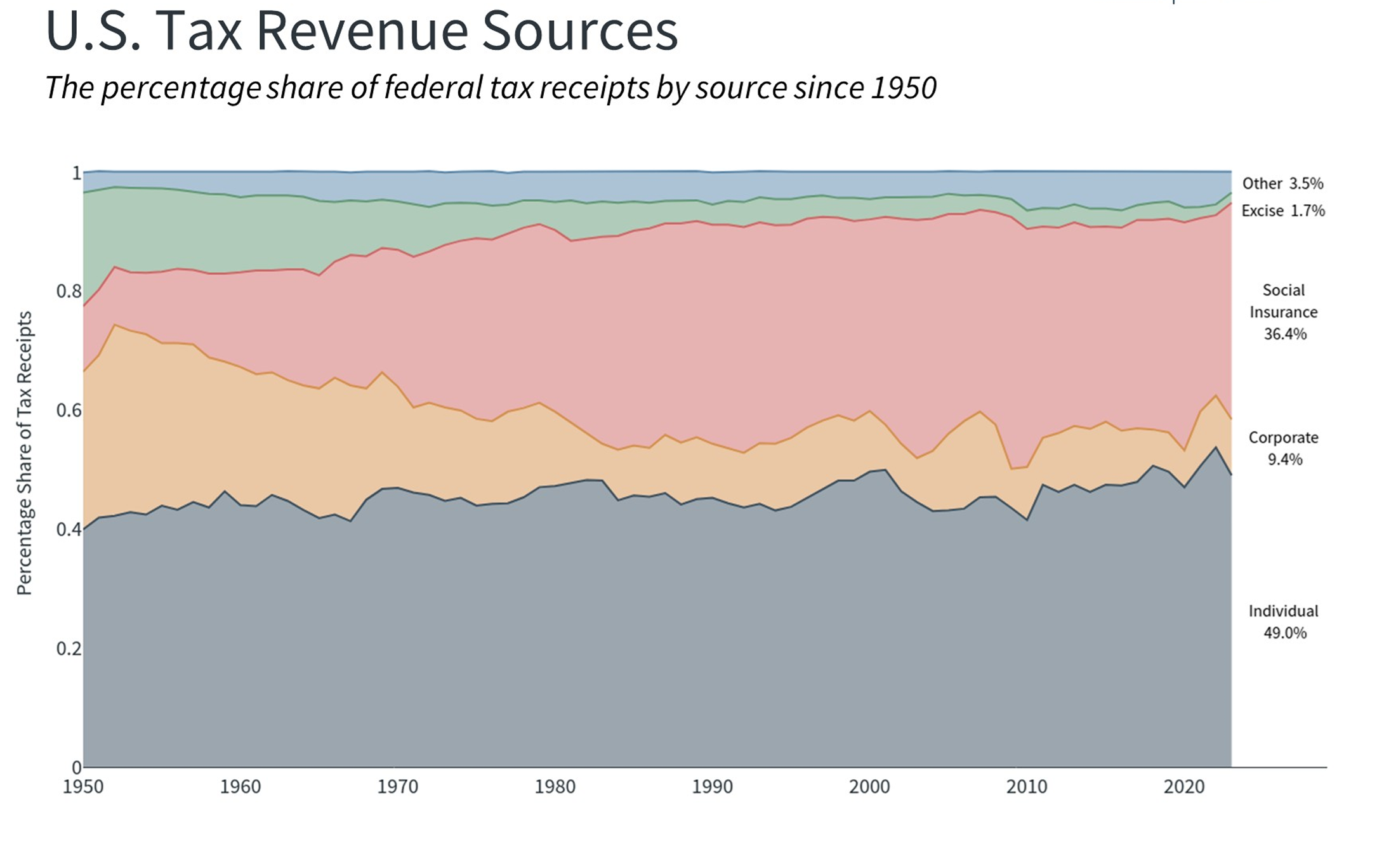

The situation has changed significantly since 1913. The chart above shows, individual income taxes now represent the primary source of federal revenue. Social insurance taxes, also known as payroll taxes, are withheld from wages and help to pay for Social Security, Medicare, unemployment insurance, and other programs. Other sources of revenue are much smaller in proportion and include corporate taxes, which were reduced by the TCJA, and excise taxes, such as tariffs.

For investors, tax policies can have direct implications on financial plans and portfolios. Over longer periods, higher debt levels can influence interest rates and inflation expectations. While these factors have been relatively high in recent years, the worst-case scenarios have not yet occurred. The key for long-term investors is to maintain portfolios that can perform across different fiscal and economic environments.

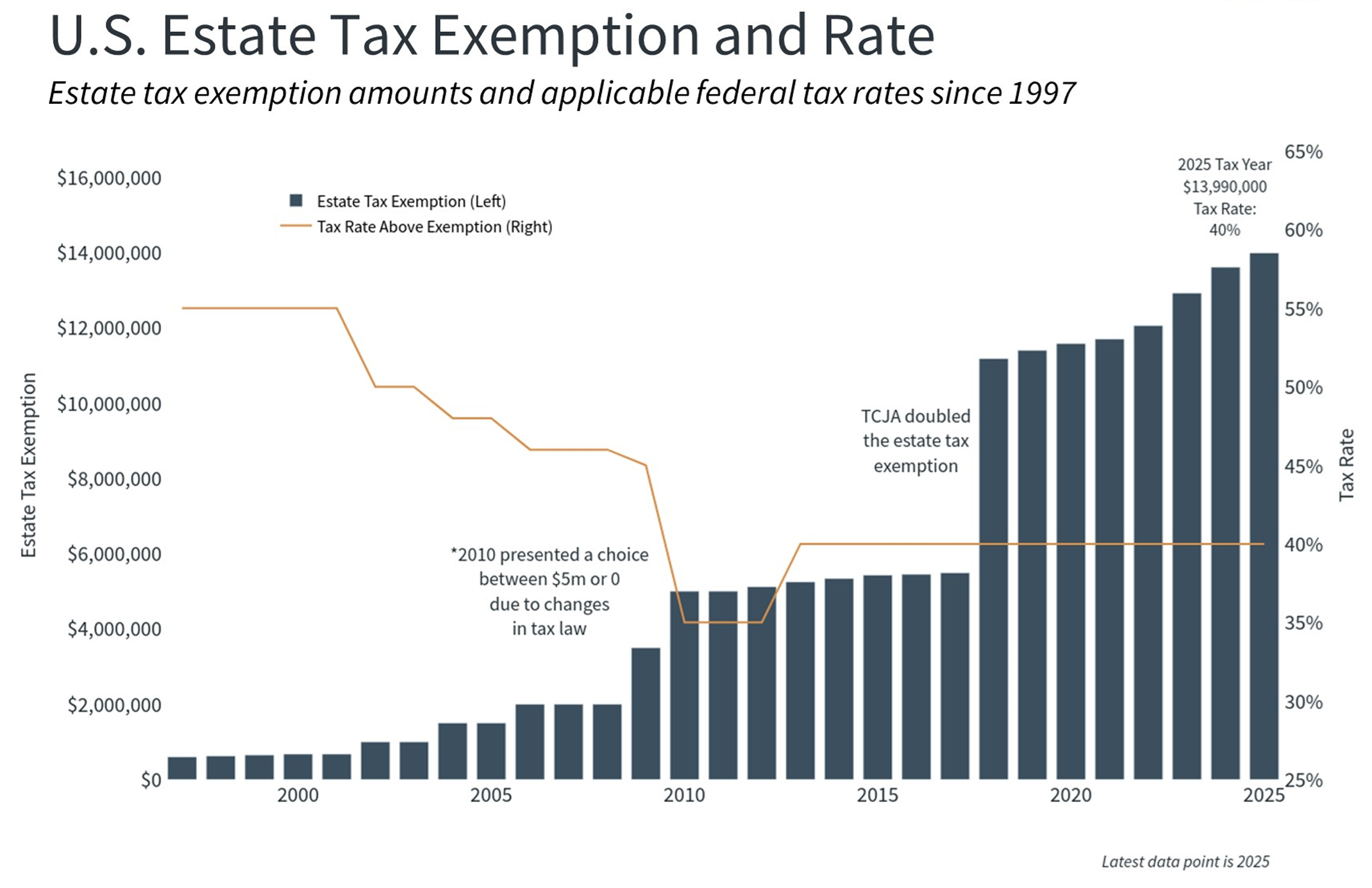

One set of provisions that would have been at the center of a tax cliff is the estate tax exemption. The TCJA doubled these limits which were scheduled to revert to previous levels this year. However, the passage of the new tax bill makes these higher exemptions permanent, further increasing the threshold to $15 million for individuals and $30 million for couples in 2026.

While it may seem like estate taxes only apply to higher net worth households, the reality is that all families must consider how assets can be passed to future generations.

The bottom line? The new spending and tax bill extends and expands the current low-tax environment. When it comes to growing deficits and the national debt, there continues to be no end in sight. The long-term investment implications for these policies are continued inflation, a weakening dollar, and a tailwind for international stocks.

Wyatt Swartz

Written 7/11/2025

With a new administration set to take control in 2025, investors are thinking about tariff policy and grappling with potential outcomes.

The greatest fear is that new broad-based tariffs will increase inflation, lead to rising interest rates, and potentially trigger a recession. If the three aforementioned were to simultaneously happen, then we’d likely repeat 2022 in capital markets. As you remember, US stocks and bonds both had double digit negative returns for the year. This was a situation that had not occurred since the 1960s.

With deceptive information being spread in media outlets, I think it is worth reviewing how/if tariffs really cause inflation. This is not a political commentary for or against tariffs. There are arguments separate from economics that could make tariffs sound/unsound policy. One might argue the merits of tariffs for geopolitical reasons, national security reasons, or as a negotiation tool. We will stick to economics.

If the intent is for economies to grow and produce at their most efficient, there would be no tariffs. Goods and services would be produced where they are most efficiently produced. Tariffs distort the natural market and create outcomes that otherwise may not have occurred and do so at different prices.

If the NFL decided it wanted the Cowboys to be more competitive with the Packers, when the two teams played, it might not allow the Packer players to not wear cleats, and gloves. Maybe the Cowboys would automatically receive the first and second half kickoffs. In this scenario, the outcome might not be different, but the final score would certainly be different, and the product (Packer performance) would be inferior for the price.

Why would any country or anyone be in favor of tariffs if they create lower quality and/or higher priced end outcomes? The quick answer is that if you are a Cowboys fan, you might care more about the Cowboys than you do about having the best, most efficient, and meritocratic outcome. The argument is that the cost of tariffs is spread across all consumers, but the benefits tend to favor lower income, lower skilled, production workers. Traditionally, democrats have been more pro-tariff because it was seen as pro-worker, republicans have typically been more anti-tariffs seeing it as anti-free market.

Enough about economics, what do tariffs mean for inflation (and markets)? Tariffs can create a one-time short-term price bump for goods/services. However, static tariff policy does not continually increase inflation, and over the long-run tariffs have no effect on inflation.

Let’s say we have Jack, and Jack has one dollar to spend. He only wants to buy two items. He buys $0.50 worth of butter, and that gets him one stick of butter. He buys $0.50 worth of ammo, and that gets him two boxes of ammo.

Then tariffs happen, but Jack still only has $1.00. Now he buys $0.75 worth of butter, and $0.25 worth of ammo. Jack still gets his one stick of butter, but now at $0.75. Jack buys $0.25 worth of ammo, but instead of getting two boxes, he only gets 1/2 a box. He spends the same total but gets less. This is the short-term bump in action. Before he got two boxes of ammo and one stick of butter for $1.00 but now, he needs $1.75 for the same goods. Inflation, right?

Not so fast my friends. Jack’s demand for butter was $0.50, and same for ammo to start with. However, his demand for ammo reduced to $0.25 when the price of butter rose. Over the longer run we know that when demand falls, prices fall too. In our example, over the long run the price of ammo would come down, because there was no increase to the money supply and the demand for ammo decreased.

The Bottom Line: Unless there is an increase in the money supply or rate of money supply expansion, tariffs alone, are not inflationary. Therefore, if interest rates rise, it is not a result of tariff policy. Tariffs can and presumably would reshape the economic playing field. Depending on what team or outcome you are rooting for, that reshaping could be positive or negative.

Wyatt Swartz

Written 12/23/2024